Open letter

The Blog Financial reform for EU citizen

For those who prefer to invest sustainably, an “ESG rating” purports to help these investors by providing an assessment of investee environmental, social, and governance policies and impacts. These ratings are intended to identify ethical investment opportunities. Aggregating E, S and G scoring is problematic however as it can allow fossil fuel companies to rank as “sustainable”. Only comprehensive reforms at EU level can repair the trust of sustainable investors.

ESG criteria are meant to enable investors to identify and invest in companies addressing sustainability risks and committed to more responsible and ethical practices. These criteria are a close cousin to credit ratings. Whereas credit rating providers assess a company’s risk of defaulting on a loan, ESG ratings providers assess a company’s integration of environmental, social, and governance criteria.

Recurring polemics and scandalsExample 1: While the high ESG rating of the residential care company Orpea was suggesting that it was meeting the highest ethical standards, independent investigation reported widespread mistreatment of residents at the Orpea owned nursing homes.

Example 2: Despite the seemingly obvious contradiction in terms, ESG investment funds keep pushing money into fossil fuel firms. about ESG ratings are raising doubts about the transparency of ESG ratings providers. Deeper analysis reveals structural issues caused by lack of consistent and transparent methodology, rather than incidents of fraud or miscalculation. ESG ratings providers now confront a growing scepticism that these ratings may be misused as a fig leaf to repair the image of polluting companies, misleading investors who want to put their money behind sustainable enterprises. Such a potentially-powerful tool for sustainable finance must not enable corporate greenwashing!

ESG criteria assess three variables:

However, instead of scoring each of these ESG parameters and reporting them separately, as differentiated scores, ESG ratings providers most often will create a composite of these parameters.

Composite ratings say nothing about the preference and priority given to each parameter’s score before the provider combines them. Doing so confuses and frustrates sustainable investors.

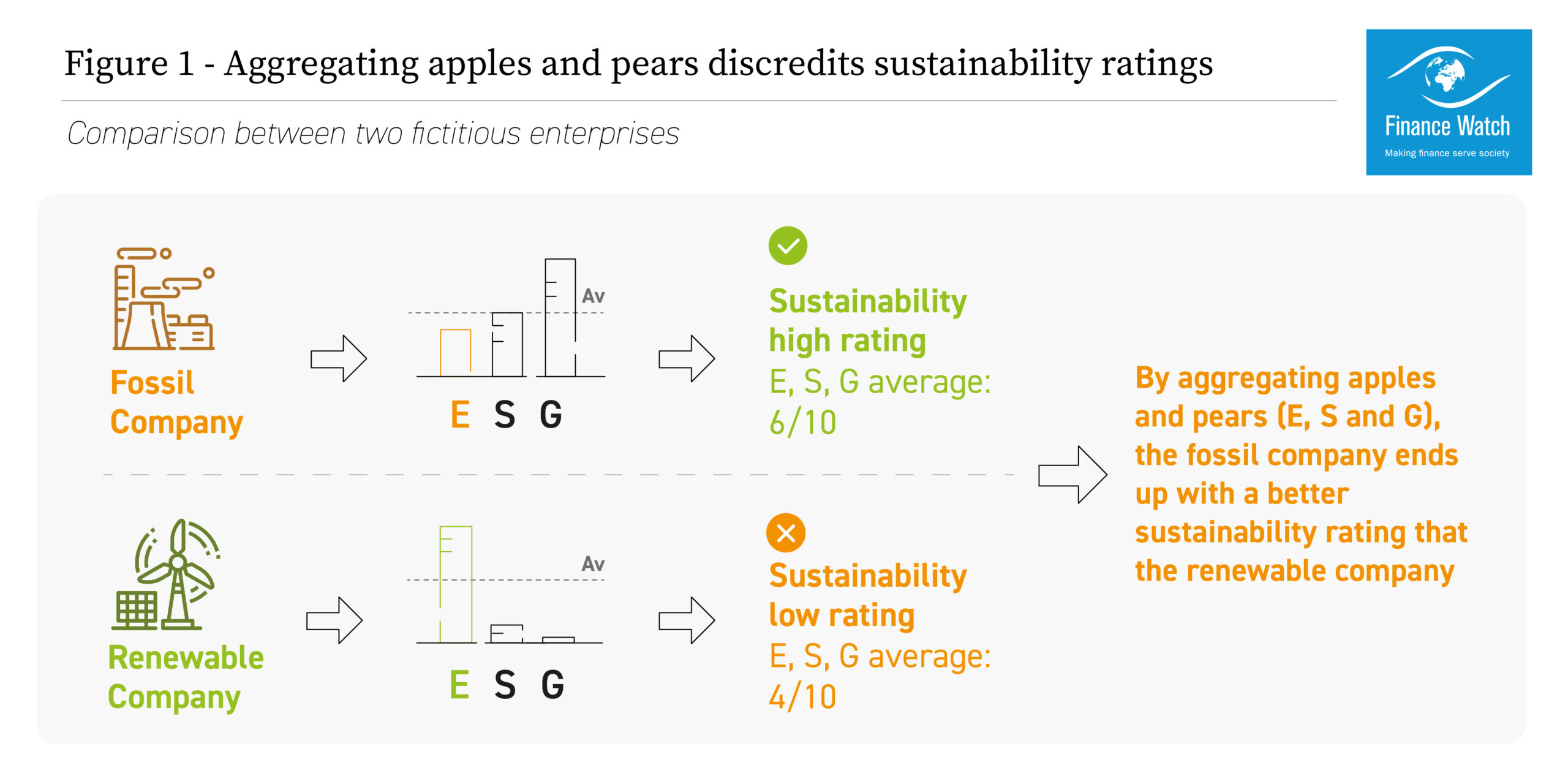

Aggregating ESG Ratings into a single composite score, therefore, results in a contradiction-in-terms. A ratings system designed explicitly to reward sustainable practices could end up awarding a high ESG rating to a company that harms the environment, simply because that company has done comparatively well in implementing good social or governance policies.

ESG rating providers use varying methods to aggregate the ESG acronym’s parameters – environmental impacts, social impacts, and governance quality of the rated company – into an aggregated score, meaning that it is virtually impossible to compare ESG scores from separate ratings providers.

One company’s score can vary considerably, depending on their ESG ratings provider and the priority given to each parameter by that provider’s particular ESG rating calculation.

When thinking of investing sustainably, civil society and consumers assume that ESG criteria assess “impact materiality” (how business activities impact communities and the environment). However, most ESG ratings providers instead assess “financial materiality” (how sustainability considerations affect businesses). The only dimension considered in most ESG ratings is the companies’ capacity to face ESG-related financial risks and to seize ESG business opportunities. Most ESG ratings, therefore, are not at all concerned with whether the rated company is doing business responsibly.

The co-existence of such radically different approaches to measuring ESG performance leads to blatant contradictions and is an obvious recipe for further misunderstandings and greenwashing accusations.

How can investors trust a rating when there is still no agreement on what exactly ESG performance is trying to measure?

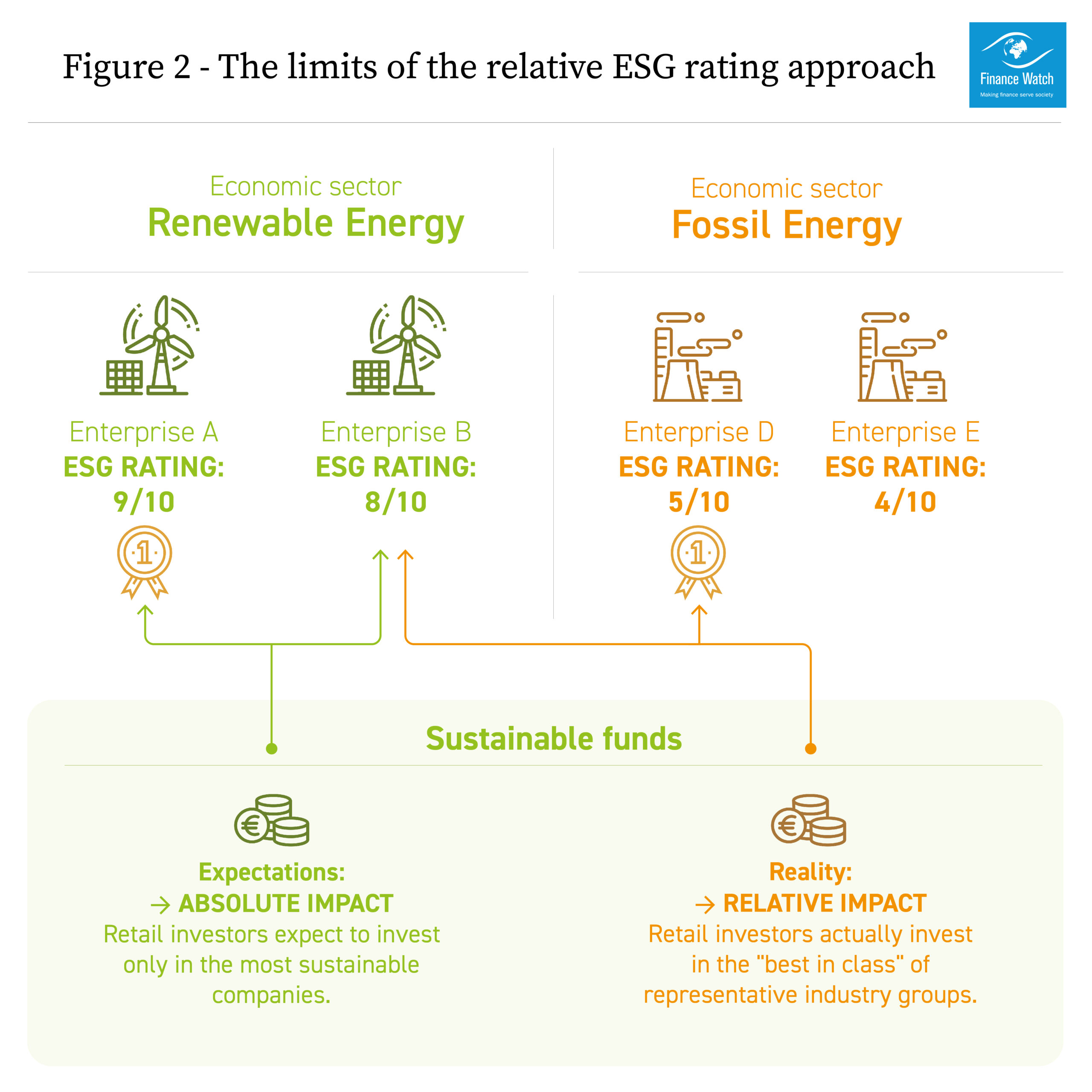

Another problem is that ESG rating agencies choose most of the time to highlight the relative ESG performance of a company rather than its absolute performance. In other words, if a given company is “Best in class” in its sector (even if it is the fossil fuel industry), it will appearFor instance, MSCI describes its assessment of a company performance as “explicitly intended to be relative to the standards and performance of a company’s industry peers" in ESG portfolios, regardless of its contribution to a sustainable world in absolute terms.

This confuses and disengages investors: focusing on relative ESG performance alone means polluting companies can still appear in ESG portfolios, sparking greenwashing accusations. Absolute performance is far more relevant for transitioning the economy to a sustainable path and better reflects the expectations of most retail ESG investors.

Moreover, within ESG rating agencies, each ESG analyst must rate a large number of companies, leaving little time to understand corporate strategies and creating a risk of gross misjudgments, like in the case of Orpea. By way of comparison, providers of more traditional market research have a ratio of analysts to companies that is five times higher.

This situation is the result of the providers’ business model and of a policy of minimizing costs in order to maximize margins. This lack of human resources limits their ability to conduct on-site visits, interview management, cross-check company statements, and therefore accurately evaluate a company’s impact on society and the environment.

ESG rating providers should not rely so heavily on companies’ public documents or on the questionnaires sent to the companies being rated. To properly assess companies’ sustainability impacts and risks, ESG ratings providers would need to employ many more analysts than they currently do. The current situation indeed raises questions about the predictive power that ESG ratings are meant to have.

Unlike credit rating providers, ESG rating providers can sell consultancy services to the very companies they rate. They are even allowed to rate their own shareholders! An absence of rules leads often to conflicts of interest. How can we trust ESG ratings providers when there is no obligation to prove independence?

A clear definition of ESG objectives is required to resolve the greenwashing controversy in the financial sector and for ESG to regain retail investors’ trust.

Clarity on the objectives of ESG ratings providers and high standards for transparency on their methodology are crucial to allow investors to sort the wheat from the chaff and invest the way they want. If Europe is to harness private finance in its path towards a sustainable economy, it urgently needs minimum standards for the market of ESG ratings.

The European Commission’s upcoming legislative proposal on ESG data and rating providers (due on 13 June 2023), is the occasion to change the rules in Europe. Finance Watch published a policy brief in May 2023 to propose clear definitions, as well as precise recommendations for the regulation of ESG ratings, in particular with regard to supervisory scope. Some of our recommendations included:

Finance Watch is a European non-profit association created to defend the public interest in the field of financial regulation. If you enjoyed this article, remember to subscribe to our newsletter and consider supporting our independent research with a tax-deductable donation.

If you work for a European NGO or as an independent expert, share our policy brief on regulating ESG rating providers with decision-makers in Brussels and consider joining Finance Watch as a member.

Pablo Grandjean

Share

Sustainable Finance

Level:Regular

30.06.2022

Sustainable Finance

Level:Expert

03.04.2023

Sustainable Finance

Level:Regular

13.12.2023

You can help tip the balance! Strengthen our impact by joining our collective efforts.